-1.png?width=50&name=Untitled%20design%20(32)-1.png)

Often considered an important indicator of our economic future, the yield curve has experienced a...

Payroll reductions by a growing list of tech companies have done little to impact the overall strength of the labor market as the Fed continues its fight against inflation

- Layoffs in the tech sector have made headlines lately, yet the unemployment rate is historically low

- Strong hiring in service industries is keeping the cost of services high, which is driving much of the remaining pressure on prices

- Further progress in the fight against inflation will depend on service sectors easing hiring to reduce labor costs in the future

As expectations for a recession increase and corporate profits lag, a growing number of companies have made headlines lately by laying off workers. Google and Spotify recently joined the long list of tech-oriented companies—Peloton, Lyft, Snapchat, Zillow, Twitter, and Facebook, among others—that have trimmed payrolls in the past year.

At the same time, the overall employment picture made a splash of its own earlier in the month with the unemployment rate for December registering at 3.5%, its lowest level in over 50 years. Jobless claims for government support are also low by historic standards, hovering near their pre-pandemic average.

The contrast between headline-making layoffs and historically low unemployment leaves some people scratching their heads and asking, what’s going on?

We typically rely on the unemployment rate as the primary measure of labor market strength, but it’s important to understand what this measure actually tells us. Simply put, the unemployment rate reveals the share of workers in the labor force who do not currently have a job but are actively looking for work.

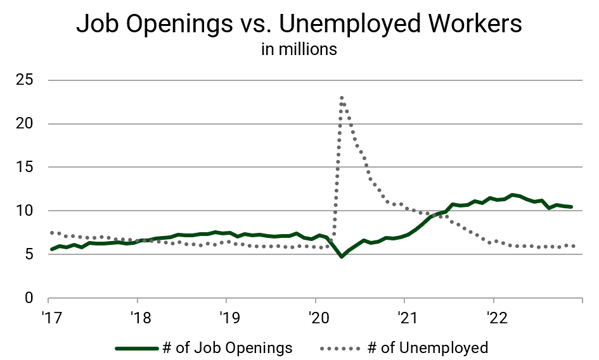

The reason the unemployment rate is low is that there are relatively few workers who are having trouble finding a job. That’s because the labor market is remarkably “tight” right now. The number of job openings currently outpaces the number of unemployed workers by nearly two to one, despite the tech layoffs that have made headlines as of late.

The chart below shows the number of job openings compared to unemployed workers, which helps illustrate the overall “tightness” of the labor market.

Source: U.S. Bureau of Labor Statistics.

It’s tempting to explain away the low number of unemployed workers by saying there are simply fewer people willing to work today, but this would be factually incorrect. Even though our labor participation rate lags behind pre-pandemic levels, there are actually more people working in the economy today than during the period of robust economic growth prior to the pandemic. The lower participation rate is due to population growth, with the addition of nearly 2 million people between 2020 and 2022.

So, the low unemployment rate is no fluke. But the labor market tightness we are seeing might not last much longer. The reason why has to do with the role that the labor market plays in the Fed’s current battle against inflation.

By law, the Fed has two main responsibilities—maximum employment and price stability. Today’s Fed has made clear that its current priority is winning the battle against inflation, even if that means slowing the economy toward a recession to do so. That means the maximum employment part of its mandate may take a back seat to price stability while the Fed has inflation in its crosshairs. It’s a classic tradeoff.

In fact, the Fed is actually hoping for the labor market to cool off for it to succeed in bringing inflation back to normal levels. The Fed is raising interest rates in hopes that this will slow economic activity and reduce inflation. And, to some extent, it has seen some progress in this effort.

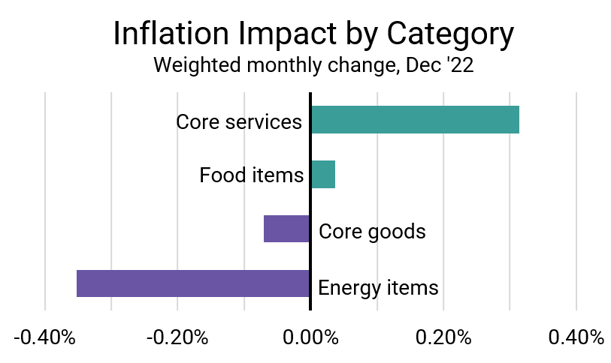

The year-over-year pace of inflation continued easing in December, but it remains high by historic standards and well above the Fed’s 2% target. In a welcome sign of progress, inflation actually declined on a monthly basis at the end of the quarter, with the CPI showing prices falling slightly from November to December.

Source: U.S. Bureau of Labor Statistics. Data are based on each category’s seasonally adjusted monthly change Nov to Dec ‘22 and relative importance for Nov ‘22.

The chart above shows that the drop in the overall price level last month was largely due to a decrease in the cost of physical goods and energy items. The remaining upward pressure on prices is coming from the rising cost of services, which is significant, as services account for over half of consumer spending.

Services are often labor intensive, so the prices of these items tend to be more sensitive to changes in labor costs. This is where the current employment picture ties into the Fed’s fight against inflation. If the Fed is to continue making progress in bringing price levels back to more typical levels, the work it has left to do lies in easing the price of services. In order to do so, the Fed is counting on hiring for service sectors to soften so that labor’s impact on the price of services will ease.

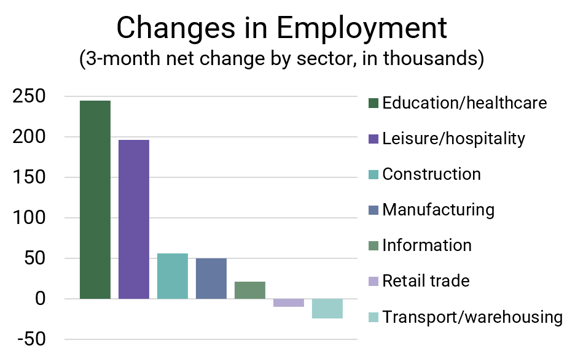

Over the last few months, hiring in service industries has been anything but soft. The chart below shows the net change in employment for some select sectors over the three-month period from October to December 2022.

Source: U.S. Bureau of Labor Statistics. Data are 3-month net change Oct-Dec ’22 by selected sector; some sectors are omitted for emphasis.

The job losses in retail trade, transportation, and warehousing shown above are largely due to consumers having pulled back on their buying of physical goods. That pullback has allowed costs for those goods to cool, helping the Fed in its fight against inflation.

But consumer spending on services has actually been increasing, driving hiring in areas such as education, healthcare, leisure, and hospitality. The increased payrolls in these service-oriented sectors are pushing wages higher for workers which translates to higher prices for services.

The takeaway from this is that the Fed has work left to do in its effort to slow the economy to reduce inflation. While layoffs for some marquee tech companies have made headlines, the overall labor market remains remarkably strong. If price levels are to continue falling to more typical levels, it will depend on service sectors easing hiring to reduce labor costs.

Markets are likely to fluctuate in the short-term as the Fed’s fight against inflation impacts the labor market, but the long-term prospects for investors to benefit from capital market growth remain strong.

.png?height=200&name=jobs%20(300%20%C3%97%20175%20px).png)